Creating a bimonthly zero based budget takes some time and thought. The good news is once you create it for the first time you can copy and paste for each month. You will have slight changes from month to month but it will be a great starting point.

If you get paid biweekly then this budgeting method will give you two extra checks a year! That is a bonus you can always count on. The checks are usually around March 15th and September 15th.

Our Story

Marriage is expensive! Just ask my husband Andrew. He was debt free when we got married and worked really hard to get that way. Andrew is a natural spender so when he got his first job with no bills he made a lot of bills for himself.

After awhile this lifestyle no longer appealed to him so he made a radical change and paid off his debt. He discovered a course by Dave Ramsey at church and completed “Total Money Makeover”. This was life changing for him. I give him a lot of credit for eating beans and rice when he did not have to, with the goal of paying off his debt as fast as possible.

However frugal I may have lived, I came into our marriage with 35,300 in debt. I had a car loan balance of 10,300 and student loans of about 25,000. Anyone with student loans knows the effort it took to graduate with so little debt.

In college I minimized what I borrowed, had scholarships, kept a job and paid as much as I could towards my student loan interest. My goal was to keep my debt as small as possible.

I have been zero base budgeting for over two decades with great success. We have been debt free since 2020. Zero base budgeting using a spread sheet is how I got started.

Monthly Budget Using Google Sheets

I created a google doc where you can create a copy in your personal google drive to customize your monthly budget. Once the google doc is open go to File > Make a Copy > OK.

You must be logged into your google account in order to save this document in your personal google drive. Once downloaded, start to edit your own private budget google doc. After you save a copy it becomes your private document.

Let's get started on your Biweekly Budget

Within the budget sheet you will find three tabs at the bottom: “Monthly Budget”, “Monthly Actual” and “Budget Items”.

The Monthly Budget spread sheet consists of a year of biweekly budget plan. There are examples for each month. We will show you how to modify the sheet to your specific needs.

The Monthly Actual spread sheet is used for the end of month reconciliation. This will be a great reference point when you make out your budget for the following year.

The Budget Items spread sheet is ideas of things that you might want to account for in different months. It serves as a checklist to make sure uncommon expenses are not forgotten.

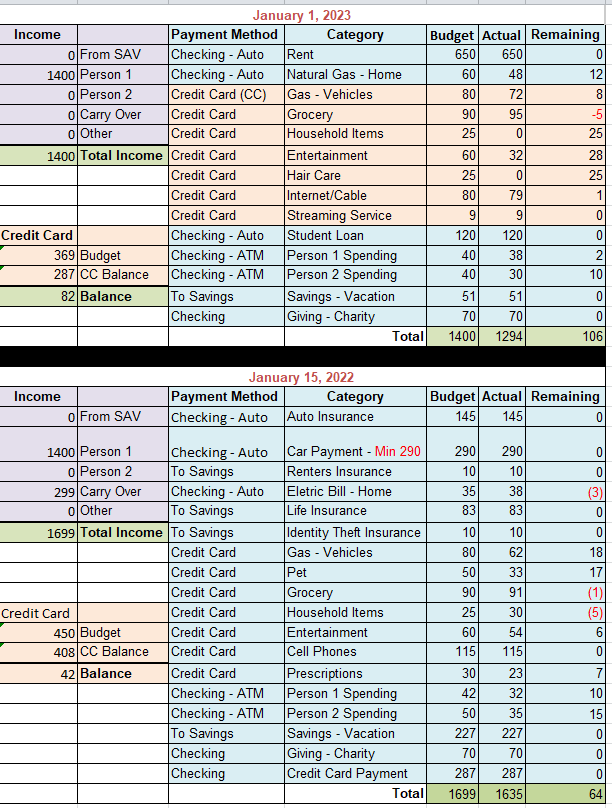

Biweekly Budget Example

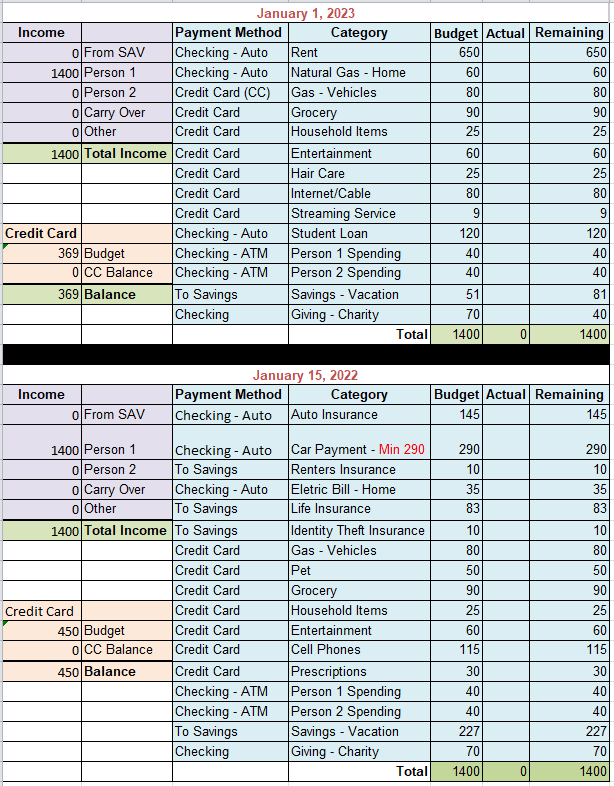

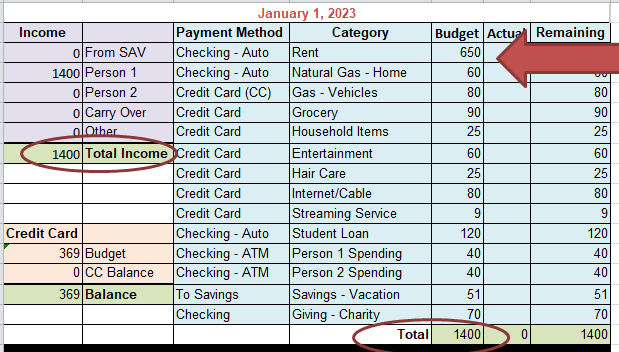

Income Section

The Income column is the amount of money brought in each month. You will enter all of the income you receive from January 1st to 15th.

- From SAV – Money from your savings account.

- Person 1 and Person 2 – The amount of money each person brought in from jobs.

- Carry Over – Amount saved from one paycheck to the next in order to ensure bills are paid in full.

- Other – Sporadic money received such as bonuses, tax refunds, gifts, etc.

Payment Method

The payment method column tracks how you pay for your bills:

- Checking Auto – Money that comes directly out of your checking account.

- Checking ATM – Cash paid items

- Credit Card – Bills or expenditures paid with a credit card.

- To Savings – Money to transfer to your savings account.

It may seem strange to track these items so granularly but it is important so you can keep track of where money is going. I often times have a large checking balance but this doesn’t mean I have money to spend. It is because I have not paid a bill such as the credit card.

Category Names

Category Names are vital to having a successful budget. They describe the money you plan to spend. Most category names are obvious. In order to have a less granule budget I group some spending items into buckets.

Example of buckets:

- Household items include: Cleaning supplies, paper products, candles, etc.

- Entertainment includes: Movies, eating out, ordering take out, taking wine to a dinner party, etc.

- Person 1 and Person 2 spending is essential. Each person should have a set amount of money they can spend on whatever they want. $40 per person every two weeks may not seem like a lot but it adds up to $160 a month which is almost 6% of the example monthly budget.

It is important to plan where your money is spent to make sure it doesn’t just disappear.

Budget Column

The Budget column is how money you will allocate to each category name from January 1st to the 15th. Some of these budget amounts are easy to come up with because they are fixed amounts each month such as: rent, mortgage, car payment, etc.

Variable budget amounts within your control take some thought and research on what you have previously spent. Spend some time analyzing these numbers and decide if they should be adjusted. These category items include: grocery, household items, entertainment, streaming services, etc.

Other budget amounts are more challenging to come up with because they change from month to month such as heat, electric, water, etc. These budget numbers are out of your control because the rates change and your consumption changes month to month.

The total of the budget column MUST match the total income. This is what qualifies as a zero based budget. Every dollar is accounted for. In this example the Total Budget is $1,400 and it matches Total Income $1,400.

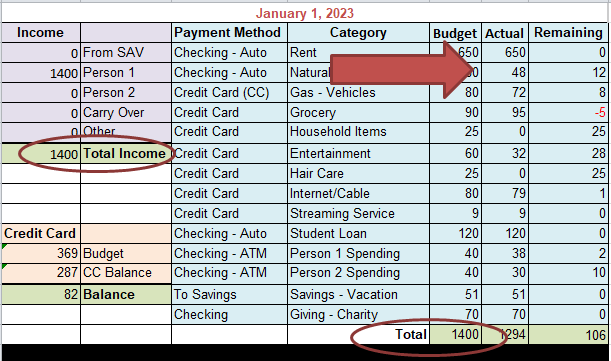

Actual Column

The actual column is how much you spend on each of these categories during the two weeks. These numbers help plan future budgets based on what you are actually spending.

I personally look at my budget and fill in the actual column weekly. This helps me stay in a “cash” mindset. I only spend what I have. If I have overspent in a category then I need to underspend in another to stay balanced.

When I am out of money in a category then I am done spending for that pay period. An example is “Entertainment”, once the money is gone then I need to find free things to do until I get paid again.

At the end of each month I total my actual spending for each category item and add it to my “Actual Monthly Spending” spread sheet. This helps me plan for each of the coming months.

Remaining Column

The “Remaining” column is money you did not spend or how much you over spent by. In this example the total remaining is $106. This means you have extra money to put towards savings or debt payments.

If this amount was negative then you would need to pull money from savings or spend less during the next pay period to make up the difference.

In this example Person 1 has an extra $2 and Person 2 has an extra $10. I roll this money forward so each person can save up for a large spending item. This is how I do it:

- I reduce my remaining amount by $12 for the January 1st – January 15th budget. Now I have($106 – $12) = $94 dollars to go towards debt or savings.

- I add $12 to my income column named Carry Over for the 15th – end of month budget.

- I increase person 1 spending to $42

- I increase person 2 spending to $50

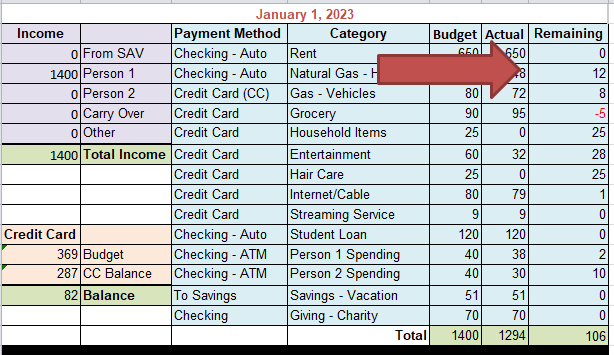

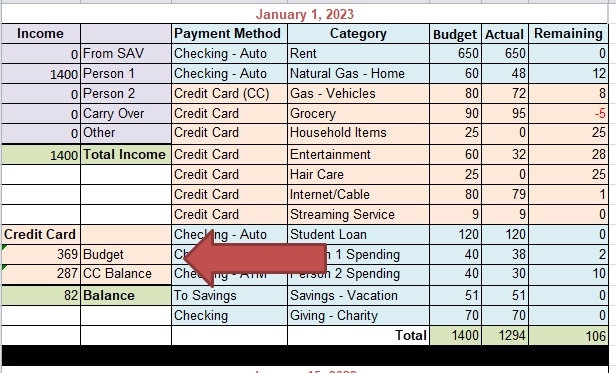

Credit Card Column

I know it is hard to keep track of a credit card. I reconcile our credit cards weekly by using the actual column in my budget. This helps me stay in control of the balance ensuring I pay them OFF monthly.

In the example above we budgeted $369 for the January 1st to the January 15th pay period. We did fantastic because we only spent $287. I keep this money set aside in either savings or as a category name in my January 15th to end of month budget.

An example of this would be adding $287 to the “Carry Over” Income column for the January 15th to end of month. Create a category name such as “Credit Card Payment” and add $287 to the budget column.

If you choose to move this money into savings create a category name in your savings such as Credit Card Payment and add $287 to your savings column.

Contrary to popular monthly payment practice, you can make multiple payments to your credit card with no penalty. I don’t know if you would get rewards by doing this (I assume not) but it might be worth the rewards sacrifice to stay on track if this is something you struggle with.

This is a perfect example of how you can use credit cards responsibly. It just takes a little preplanning and restraint.

End of month budget example:

Let's talk about what you see above

In this example January 1st pay period was positive by $106. I started the January 15th to end of month with $299 from the previous month. This consisted of:

- $2 for Person 1 making their starting balance $42

- $10 for Person 2 making their starting balance $50

- $287 for Credit Card Payment. I created a new category name and added this amount to the budget column.

The Total Income for the January 15th to end of month is now $1699. After putting in all of my category items and budget amounts the total budget column totaled $1699. This is a zero balance budget. Every dollar is accounted for.

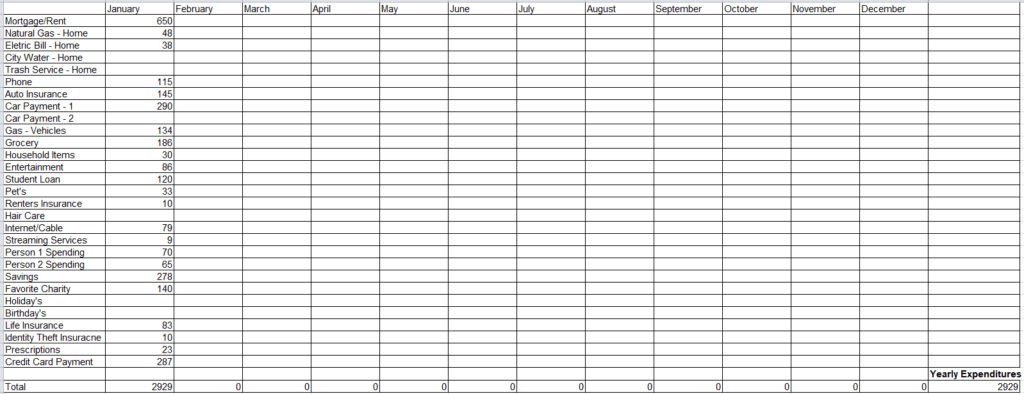

Next take the time to complete the “Actual Monthly Spending Spread Sheet”. This will make your future budget planning a breeze. You can quickly look at the previous month or the previous year to help guide you in building your budget in minutes.

Actual Monthly Spending Spread Sheet

A budget requires adjustments

I use this spread sheet to track our actual monthly spending. Without this snap shot I would not know what I typically spend in each category each month. It would make it impossible for me to set a realistic budget each month. I analyze our spending categories every 3 months to see if I need to make changes to our budget amounts.

If you find that you are consistently going over or under in a category such as grocery then you will need to adjust your budget to how you are actually spending versus how you “ideally” want to spend. Sometimes these changes are not within our control an example of that is inflation.

When you create your budget for the first time you will have success and failure but with this sheet you will get it down to a science year after year. The trick is not to give up! You only fail if you don’t try.

Let's talk about if our budget went poorly for the month

Yes, it happens. A budget is an educated guess based on previous data, but it can never be exact because the future has not happened yet. This is why no one should place guilt on themselves for not staying perfectly within the boundary they set.

Maybe you got sick with strep throat and had an unexpected doctor visit with a prescription you were not counting on. Maybe you hosted a dinner party. Maybe you had an extra drink at the bar.

Life happens and you need to live it. However, going over the budget does have consequences such as not paying extra principal towards debt, not having savings, not having entertainment money for the next pay check, etc. Building in consequences is motivation to stick to your budget as much as possible with the result of getting ahead and having a healthy financial future.

Let's talk about giving

I think giving is an important category because so many people need our help. If you don’t have money to give then don’t, but if you have extra it is important to help other people, charities, church’s, communities, etc. We are lucky to live in a country with so many luxuries and sometimes we forget there are people suffering here as well. It never seems like enough, so most people forgo the practice of giving. The truth is a little goes a long way and can make a very big impact.

Something else to think about if you can’t give money then give some of your free time. There are a lot of organizations that can use your skill set to benefit others around you.

Conclusion

Know your monthly income and don’t spend what you don’t have. Make a plan and follow it the best you can. You will be successful if you live within your means. Creating your fist budget will take you a bit of effort but living within your means is worth it! Keep coming back to your budget. The process will get faster and faster. Checking in weekly is the key to staying on budget.