Zero based budgeting is the best method I have found to keep track of my debts and build a managed savings account. I started my first zero budget spread sheet in college. At that time I did not use credit cards.

Zero based budgeting is where you take your income then subtract all of your expenses and savings leaving the balance zero. Scary right? Not really, you get used to it very quickly.

I have lived on a budget where after all my bills were paid, I had about $20 for food that needed to stretch for two weeks. Ouch! This taught me a lot about not having food waste and cooking in bulk.

My Story

I was in college working part time and going to school full time with rent, utilities, car insurance, gas, books, etc. as bills. I had a choice to make. I could go full time at my job and continue with school full time at night or ask my parents for help.

Fate intervened in this case because my mom came to visit me. We live about 200 miles apart. I was at work when she arrived and went looking for a snack. Ha! What she found was minute rice, peanut butter, canned beans, and ramen noodles.

Next, she went to the refrigerator where she found mayo, ketchup, mustard, and a pitcher of Britta water. I was not around for her frenzied freak out but she informed me later quite thoroughly.

My mom went to the store and bought enough to fill my cupboards with staples such as bread, pasta, canned vegetables, etc. and my refrigerator with a few basics such as milk, butter, cheese and lunch meat.

She went home and told my father the way I was living and after dinner that night he took their leftovers and put them in the freezer. My mom asked him what he was doing and he said, “feeding Christin”.

I visited a couple of weeks later and to my surprise I had a cooler full of leftover meals to take home with me. We lived like this for a couple of years and then my car gave out. I opted to work full time and finish my last bit of school at night so I could afford a new car and food.

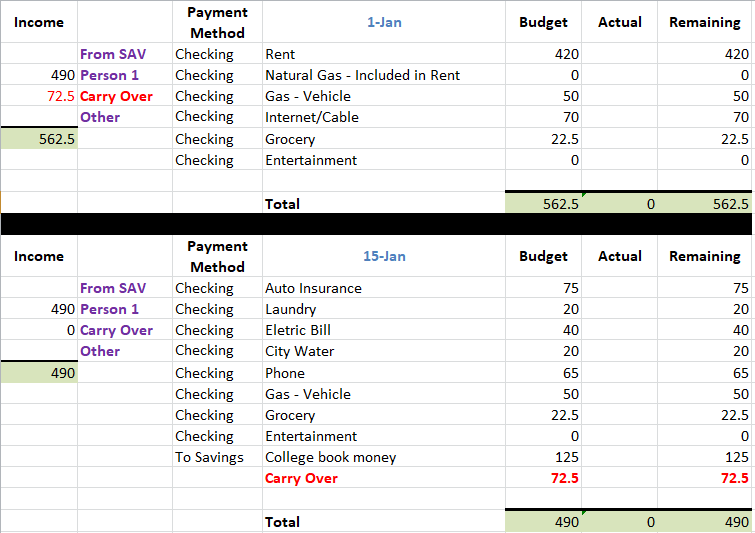

This was my first budget at the beginning of the month:

I found that working with spread sheets was the best method for me. I wrote down all of my expenses for the month and then broke the expenses into two different pay periods. I discovered I did not make enough to meet the first of the month bills so I needed to save money from my second check in order to be able to pay the first month bills. I called it “Carry Over”.

I knew that no one was ever going to see this budget sheet but me so I was completely honest about what I was spending. This could be hard sometimes because I am the type of person that would shame myself if I don’t stay on budget. I had to learn how to accept I was never going to be able to budget perfectly. Life is more spontaneous than I gave it credit for.

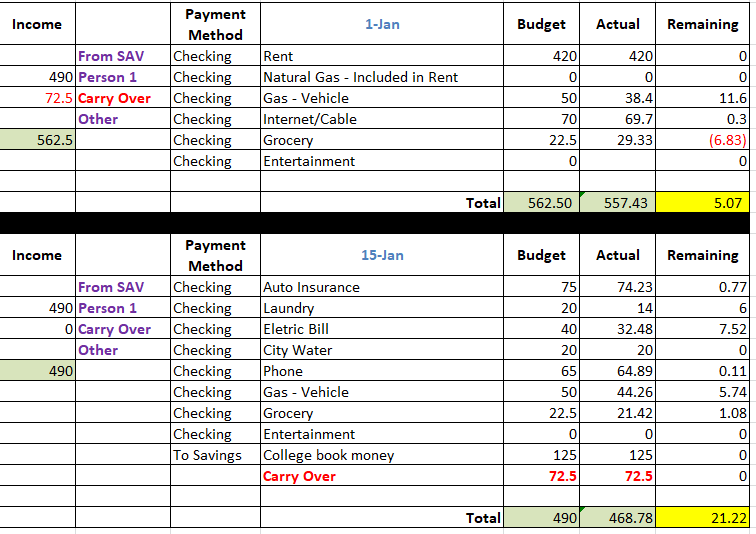

On my journey to accepting what I actually spent I made a column “Actual” and was completely honest about what I spent. I quickly learned by being honest with myself I could budget easier because I could see what I was actually spending versus what I had planned to spend.

End of month budget example:

In this example I came out ahead for the month. I would add up the $5.07 and $21.22 and place the total $26.29 into my savings account. I would usually spend this money on “Entertainment” eventually. Sometimes this extra money was pulled from savings when I had a bad month and “blew the budget”.

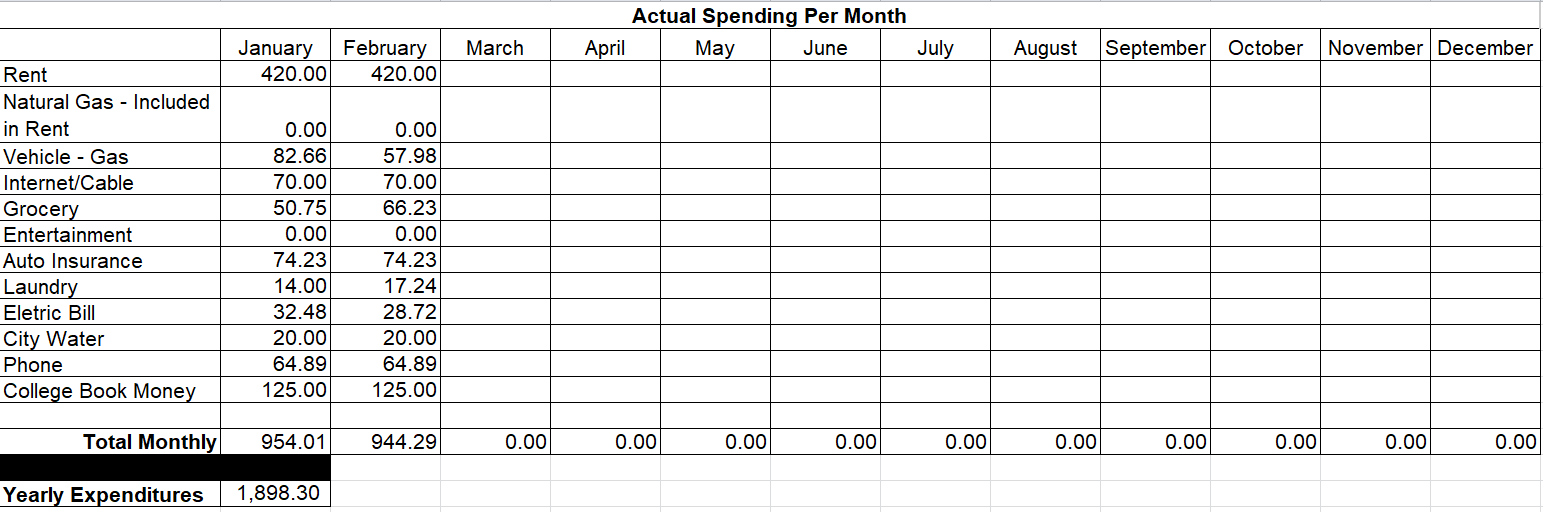

Below is another great budgeting tool I created to help my future budgets. I used this actual monthly spending spread sheet to track my monthly spending for the year. As time went on I built up a lot of data around my spending habits. The data allowed me to budget each month based on what I spent in that month the year before. This was great because it meant building my monthly budget was super easy.

Actual Monthly Spending

Starting life with a limited income and accumulating debt from school taught me a lot about how to be frugal and to appreciate every dollar that I earned. I did not know what a zero based budget was when I started budgeting. I just wrote down my bills until I ran out of money. It did not take long.

I am fortunate that as I age through life my income has grown at a faster rate than my expenses but I still budget every dollar I make. I make sure 15% goes into my retirement, 5% into other investments and I cover my bills.

It is funny when people look at the success of my scrimping and saving and instantly think it came overnight but the truth is it took decades to become as financially independent as I am. I still scrimp and save including shopping deals, using coupons, and buying vacations on a discount. There is no need to spend extra money just because it is there. You never know when you are going to need it.

Try it yourself!

I created a google doc where you can create a copy in your personal google drive to customize your monthly budget. Once the google doc is open go to File > Make a Copy > OK.

You must be logged into your google account in order to save this document in your personal google drive. Once saved, start to edit in your own private google doc. Please note once you make a copy I cannot see it so don’t be nervous because your information is NOT on display for the world to see!